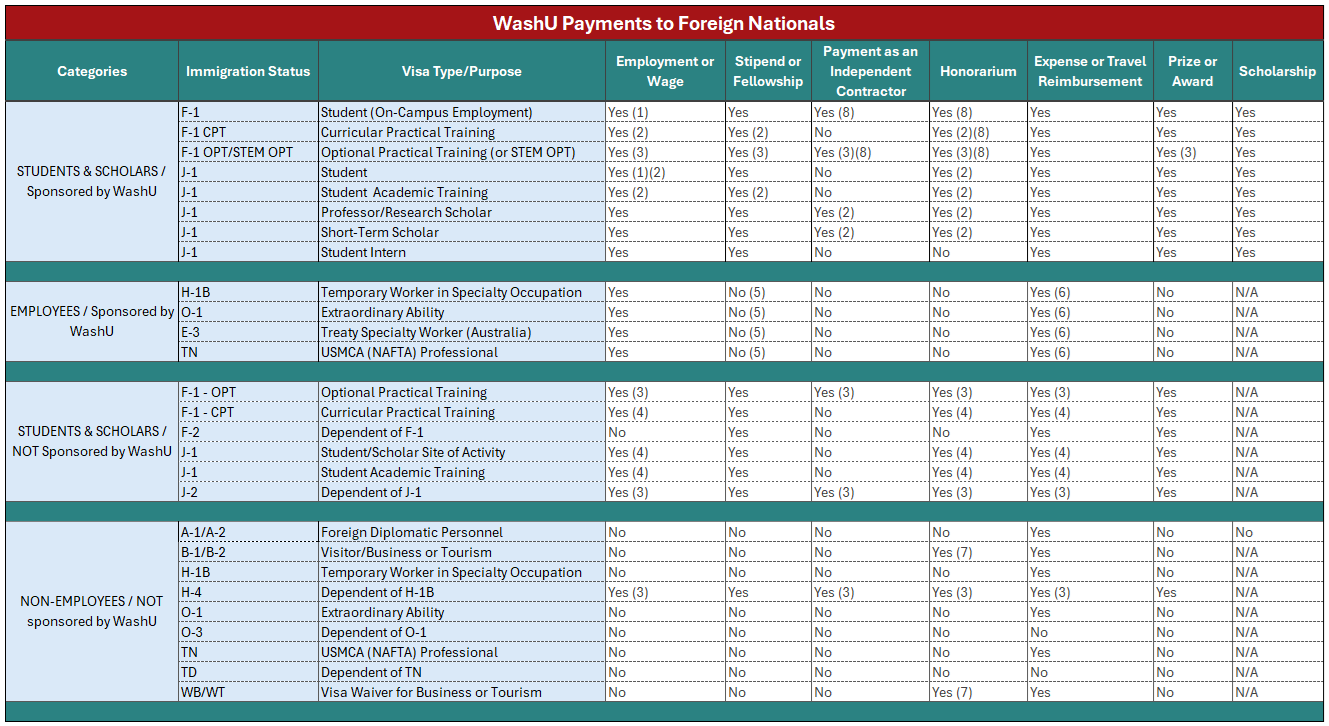

This page and chart below provide guidance on WashU payment policies for foreign nationals, based on immigration status and visa type. The chart specifies allowable payment types, including wages, stipends, independent contractor payments, honoraria, travel reimbursements, prizes/awards, and scholarships.

The chart and the explanation are important because they serve as a single, authoritative guide to ensure WashU complies with two complex areas of federal law: U.S. immigration and U.S. tax (IRS) regulations. Incorrect payments to foreign nationals can result in severe legal consequences for both the university and the individual.

Disclaimer statement

The Office for International Students and Scholars (OISS) provides resources and content for general informational and educational purposes only. This information does not constitute legal advice or tax advice. The information provided is subject to changes in the law. It is the foreign national’s responsibility to maintain their immigration status and to ensure that they have proper authorization or approval to accept a payment. If a foreign national believes they are eligible for a payment that is listed as “No” in the chart, or if they have any specific legal questions, we encourage them to seek personalized legal advice from a qualified attorney at their own discretion and expense.

Notes

(1) Limited to 20 hours per week during Spring and Fall semesters; full-time allowed during breaks if the student will enroll in coursework in the following semester

(2) Requires written authorization from WashU OISS (the foreign national must contact OISS)

(3) Requires written authorization from USCIS (i.e. EAD)

(4) Requires written authorization from OISS at sponsoring institution

(5) H-1B, O-1, E-3 or TN employees cannot receive direct external funding from third parties. However, if the funds are awarded to support research activities performed as part of the faculty member’s responsibilities as detailed in the employee’s H-1B, O-1, E-3, or TN status petition, then the funds can be administered through the University. Refer to Sponsored Projects Accounting for more details.

(6) H-1B, O-1, E-3 and TN employees may receive direct reimbursement for travel expenses associated with occasional speeches, lectures, conferences or consultations at other institutions or organizations if these activities are incidental to the H-1B, O-1, E-3 or TN employment. Reimbursement should be accepted only for travel expenses actually incurred by the employee.

(7) Subject to the requirements of the 9/5/6 rule, foreign nationals in B-1, B-2, VWB and VWT status may accept an honorarium and/or reimbursement of travel expenses for “usual academic activity or activities” if spending 9 days or less at WashU and if the individual has accepted such payment from no more than 5 educational or research institutions (including WashU) in the previous 6-month period.

(8) Requires OISS verification prior to beginning of activity via the OISS Miscellaneous Payment Verification Form.

Understanding payment categories

| Chart Category | Definition |

|---|---|

| Immigration Status | F-1, J-1, H-1B, O-1, E-3, TN, etc. |

| Visa Purpose | Student, Professor, Research Scholar, Intern, Temporary Worker |

| Payment Types | Employment/Wage, Stipend/Fellowship, Independent Contractor, Honorarium, Expense/Travel Reimbursement, Prize/Award, Scholarship |

How to use the chart

- Identify the sponsor of the foreign national.

- Questions to ask the foreign national – Who is the sponsor of your immigration/visa status? Or who issued your document, which identifies you as a foreign national in the U.S.?

- The foreign national will either be sponsored by WashU or another institution.

- Identify the foreign national’s immigration status that will be active when a payment is made.

- Narrow down their specific purpose for the activity in question.

- Some immigration statuses are listed more than once because the answer depends on the foreign national’s specific purpose for being in the U.S.

- For example, a J-1 Exchange Visitor may be in the U.S. for different reasons, and it is the reason itself that sometimes determines whether they can receive a certain payment.

- Identify the type of payment in question and refer to the Definitions above for details.

Definitions

The definitions below refer to column headers within the chart.

As per the Immigration Reform and Control Act (IRCA), I-9 employment refers to “any service or labor performed by an employee for an employer within the U.S.” An employee is defined as “an individual who provides services or labor for an employer for wages or other remuneration but does not mean independent contractor.” (8 CFR 274a)

A stipend refers to a specific type of payment and how it’s categorized for tax purposes. At WashU, stipends are classified as taxable scholarships provided for living expenses and are not payments for services rendered.

These payments are processed through accounts payable, typically as a miscellaneous payment request or a Supplier Invoice Request.

For a special, non-recurring activity or event also known as “a usual academic activity.”

Per diem is not recommended for expense and travel reimbursement. As a best practice, reimbursement should only be for actual expenses accrued or follow the GSA per diem rates.

A payment in recognition of accomplishment; not a service rendered in exchange for compensation. Includes study participation.

Understanding the answers

You will see one of 4 types of answers in the matrix:

- “Yes” – activity and payment for the activity is always allowed for a foreign national in that category.

- “Yes (#)” – activity and payment for the activity is sometimes allowed; additional stipulations, considerations and requirements exist; see the Notes section below the chart for details.

- “No” – activity and payment for the activity is never allowed for a foreign national in that category.

- “N/A” – this type of activity or payment is not applicable for the foreign national in this category.

In many cases, the matrix indication is applicable to both the payment and the activity associated with that payment. This chart considers both the immigration and the tax compliance side of the question.

The chart is meant to simplify complex immigration and tax information. Therefore, straightforward Yes/No answers may not always be possible for specific questions or situations. The Notes section addresses this complexity.

Important!

Review and understand any notes linked to a “Yes” response.

For example, a J-2 Dependent may receive wages only with written authorization from USCIS, indicated as “Yes(3)” in the matrix. Accepting employment without this authorization violates the J-2’s immigration status, which can lead to serious consequences such as deportation and future ineligibility to enter the U.S.

Distinguishing between a “Yes with a note” and a “No” is crucial for both the individual and the institution responsible for the payment.

Additional resources

OISS is here to assist you with interpreting the chart and answering questions. Email OISS at oiss@wustl.edu if you:

- do not see a visa type or payment type that applies in your case

- do not understand any portion of the chart or the notes

- do not understand the reasoning behind an answer

- are unclear on how to proceed after determining the answer

OISS may re-direct your question to the Tax Department if necessary.

Frequently asked questions

- Why are some payments unallowable? Unallowable payments typically result from federal immigration laws, IRS regulations, or university risk management policies.

- What documentation is required for allowable payments? Documentation requirements vary depending on visa type, purpose, and the type of payment in question.

- Whom should I contact for guidance? First contact OISS with questions about the information presented on this page or the chart. If necessary, OISS will refer you to WashU HR, Tax Department, Office of General Counsel, or Payroll Services.